Private Credit vs Corporate Bonds: For many years, discussions about fixed-income investing were relatively straightforward. Investors seeking income and diversification typically allocated capital to government bonds, investment-grade corporate debt, or high-yield bond funds depending on their risk tolerance and return objectives. While these assets remain important components of many portfolios, the investment landscape has become increasingly diverse over the past decade.

One of the most significant developments has been the rapid growth of private credit. Once considered a specialist strategy used primarily by large institutions, private lending has evolved into a major segment of global capital markets. Pension funds, insurance companies, endowments, sovereign wealth funds, and family offices have steadily increased their exposure to private credit, viewing it as a potential source of income, diversification, and long-term returns.

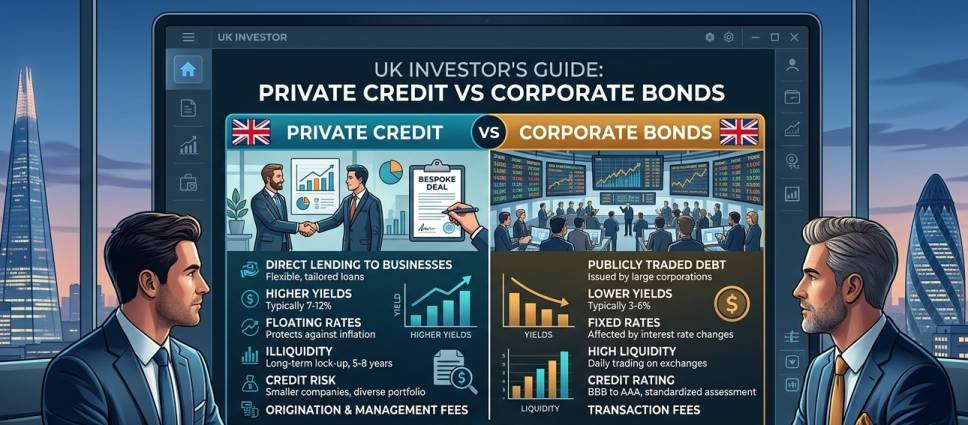

The expansion of private credit has inevitably led to comparisons with corporate bonds. Both involve lending capital to businesses in exchange for interest payments, yet the similarities largely end there. The two asset classes operate within different market structures, offer different liquidity characteristics, and present investors with distinct opportunities and risks. Understanding those differences is essential because the debate surrounding private credit versus corporate bonds is often framed too narrowly around yield, when the more important considerations frequently involve liquidity, transparency, portfolio construction, and investment objectives.

The Changing Structure of Corporate Lending

The growth of private credit cannot be understood without examining how corporate financing has evolved since the global financial crisis. Regulatory reforms introduced after 2008 significantly altered the banking sector, encouraging banks to strengthen balance sheets and reduce exposure to certain forms of lending. While these changes were intended to improve financial stability, they also created opportunities for alternative lenders to provide financing that traditional institutions were becoming less willing or less able to offer.

As a result, private investment firms increasingly stepped into areas of the market that had historically been dominated by banks. Rather than issuing publicly traded bonds, many businesses began securing funding through privately negotiated lending arrangements. Over time, these transactions developed into a substantial market that now plays an important role in corporate finance across multiple sectors and regions.

This shift does not mean that public bond markets have become less relevant. Corporate bonds continue to represent one of the most important funding mechanisms for large companies and remain a core holding for countless institutional and retail investors. What has changed is that investors now have access to a broader range of lending opportunities than was available a generation ago, creating new choices when constructing income-focused portfolios.

Why Liquidity Deserves More Attention Than Yield

One of the most common mistakes in discussions about private credit is the tendency to focus almost exclusively on yield comparisons. While income remains an important consideration, it rarely tells the entire story.

Liquidity often receives less attention because it is difficult to appreciate its value when markets are functioning normally. During stable periods, investors may view liquidity as a feature they are unlikely to need. However, market history repeatedly demonstrates that liquidity becomes far more valuable during periods of volatility, economic uncertainty, or unexpected changes in personal circumstances.

Corporate bonds generally provide greater flexibility because they trade in public markets. Investors can typically buy or sell positions without waiting for a loan to mature, allowing portfolios to be adjusted as economic conditions evolve. The ability to react quickly to changing circumstances has long been one of the defining advantages of publicly traded debt markets.

Private credit operates differently. Investors generally commit capital for longer periods and may have limited opportunities to exit before underlying loans are repaid. The additional income associated with private lending is partly a reflection of this reduced liquidity. In practical terms, investors are compensated for accepting restrictions that do not usually exist in traditional bond markets.

The significance of this trade-off depends entirely on the investor. For institutions with multi-decade investment horizons, reduced liquidity may be a manageable compromise. For investors who prioritise flexibility or anticipate future capital requirements, liquidity itself may represent a meaningful source of value.

A Practical UK Example

The significance of liquidity becomes clearer when viewed through a practical investment scenario.

A UK pension fund with a 20-year investment horizon may be comfortable allocating a portion of its portfolio to private credit because immediate access to capital is not essential. Long-term liabilities allow pension schemes to focus on income generation and diversification without requiring daily liquidity across every asset.

An individual investor who expects to access portfolio assets within the next five years may reach a different conclusion. Even if private credit offers attractive income opportunities, the flexibility provided by corporate bond funds may prove more valuable because future spending requirements are less predictable.

Neither approach is inherently superior. The most appropriate choice depends on the investor’s objectives, time horizon, and liquidity requirements.

Transparency and Market Pricing Matter More Than Many Investors Realize

Another important distinction between private credit and corporate bonds involves transparency. Public bond markets provide continuous price discovery, allowing investors to observe how securities are valued in real time. Credit ratings, financial statements, analyst research, and market pricing collectively create a relatively transparent environment in which investment decisions can be evaluated and monitored.

Private credit does not operate under the same framework. Because transactions occur privately, information is often less accessible and valuations are typically updated less frequently. This does not necessarily make private credit more or less risky, but it does create a different investment experience. Investors may have less visibility into short-term market fluctuations and greater reliance on the expertise of fund managers responsible for originating and monitoring loans.

Supporters of private credit frequently argue that this reduced exposure to daily market sentiment can be beneficial, particularly during periods of heightened volatility. Critics counter that less frequent pricing does not eliminate risk but simply makes it less visible. Both perspectives contain elements of truth, which is why investors should understand how valuation methodologies differ before comparing the two asset classes directly.

What UK Wealth Managers Are Watching in 2026

Within the UK wealth-management industry, private credit is increasingly viewed as a portfolio-construction tool rather than simply a higher-yielding alternative to corporate bonds.

Professional advisers are paying closer attention to factors such as manager quality, portfolio diversification, borrower strength, liquidity terms, and the interaction between private assets and traditional holdings. The conversation has moved beyond identifying the highest-yielding asset and toward understanding how different investments contribute to overall portfolio resilience.

This reflects a broader trend within wealth management. Investors are increasingly seeking multiple sources of return rather than relying heavily on a single asset class. Private credit is often discussed as part of a diversified strategy rather than as a replacement for traditional fixed-income investments.

Why Institutional Investors Use Both Asset Classes

Media coverage occasionally presents private credit as a challenger poised to replace traditional bond investing. In reality, the investment decisions made by large institutions suggest a more balanced perspective.

Most pension funds, insurance companies, and diversified asset managers continue to maintain significant allocations to corporate bonds while gradually increasing exposure to private credit. This approach reflects a recognition that the two asset classes serve different purposes within a portfolio.

Corporate bonds provide liquidity, transparency, and broad market exposure. Private credit can introduce alternative return streams and access to opportunities that may not be available through public markets. When used together, they can create a more diversified fixed-income allocation than either asset class could provide independently.

This is an important distinction because it shifts the discussion away from identifying a single winner. Portfolio construction is rarely about selecting one asset at the expense of all others. Instead, successful long-term investing often involves combining assets with different characteristics in ways that support specific objectives and risk tolerances.

The Role of Risk in the Comparison

Any comparison between private credit and corporate bonds must acknowledge that risk cannot be assessed through yield alone. Higher income opportunities are frequently accompanied by additional complexities that deserve careful consideration.

Private credit investors face risks related to borrower performance, portfolio concentration, manager selection, and limited liquidity. Corporate bond investors face risks associated with interest-rate movements, credit deterioration, inflation, and market volatility. The nature of these risks differs, which makes direct comparisons difficult without considering the broader context of an investor’s portfolio.

Rather than asking which asset class is safer, a more useful question is how each source of risk aligns with an investor’s objectives and constraints. Risk is not simply something to avoid; it is something to understand and manage. The most appropriate investment often depends less on the characteristics of the asset itself and more on the circumstances of the individual or institution allocating capital.

Looking Beyond Headlines

The increasing attention given to private credit reflects genuine changes within global capital markets, but headlines can sometimes oversimplify a far more nuanced reality. The growth of private lending does not signal the decline of corporate bonds, nor does it mean investors should abandon traditional fixed-income strategies in favour of alternatives.

What it does demonstrate is that investors now have access to a wider range of tools for generating income and diversifying portfolios. Private credit and corporate bonds each offer distinct advantages, and their usefulness depends largely on how they are incorporated into a broader investment strategy.

For UK investors evaluating long-term portfolio allocations in 2026, the most productive approach may be to move beyond the idea of choosing between private credit and corporate bonds. The more relevant question is how each asset class can contribute to a resilient portfolio capable of navigating different economic and market environments over time.

Private Credit vs Corporate Bonds: Comparing Key Characteristics

| Factor | Private Credit | Corporate Bonds |

|---|---|---|

| Market Structure | Private lending arrangements | Public debt securities |

| Liquidity | Generally limited | Generally higher |

| Pricing | Periodic valuation | Continuous market pricing |

| Transparency | Lower | Higher |

| Accessibility | Often through specialist funds | Widely accessible |

| Investment Horizon | Typically longer-term | Flexible |

| Portfolio Role | Alternative income source | Core fixed-income allocation |

Frequently Asked Questions

Why has private credit grown so rapidly?

The market expanded as non-bank lenders increasingly filled financing gaps created by changes in traditional banking practices while investors searched for diversified sources of income.

Does private credit always produce higher returns than corporate bonds?

No. Returns vary depending on credit quality, economic conditions, fees, manager expertise, and portfolio construction.

Why do investors accept lower liquidity in private credit?

Many investors are willing to sacrifice liquidity in exchange for access to lending opportunities that may offer higher income or diversification benefits.

Are corporate bonds still relevant in 2026?

Yes. Corporate bonds remain an important component of many institutional and private portfolios because of their transparency, accessibility, and liquidity.