VCTs vs EIS: Venture Capital Trusts (VCTs) and the Enterprise Investment Scheme (EIS) are both ways to invest in fast‑growing but riskier UK small and medium‑sized businesses while saving on tax. However, they work very differently if your main goal is to grow your capital. In 2026, EIS usually gives you a bigger upfront tax break and is better suited for aiming at high capital growth. VCTs, especially after April 2026, are more focused on diversified, professionally managed funds that pay tax‑free income and come with a smaller headline tax relief.

Important: Both VCTs and EIS involve investing in high-risk, early-stage businesses. Capital is at risk, and investors should seek independent financial advice before investing.

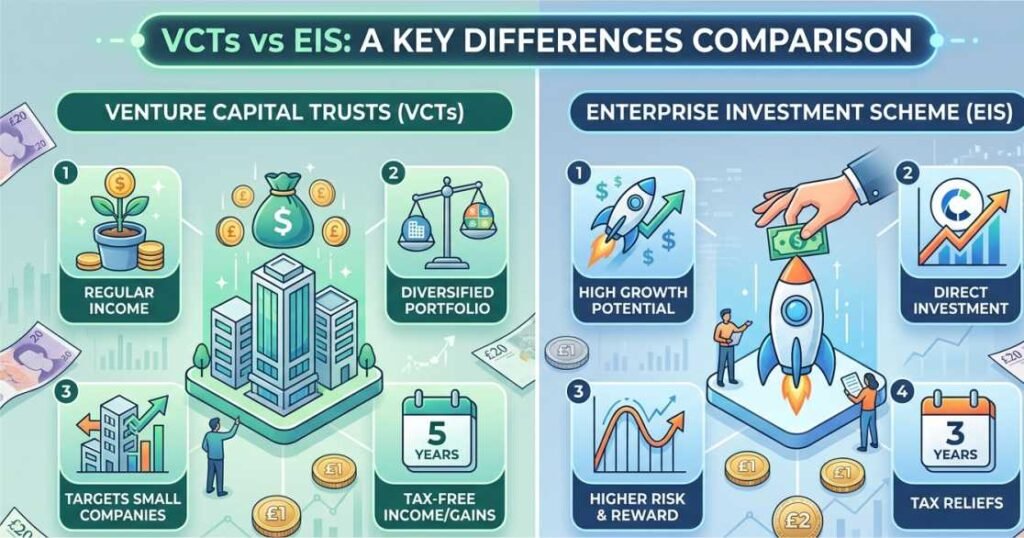

What are VCTs?

Venture Capital Trusts pool investor money into a diversified portfolio of small, unquoted UK companies, managed professionally like a fund. Shares trade on the London Stock Exchange, providing liquidity compared to direct investments.

Unlike EIS, investors do not select individual companies. Instead, experienced fund managers make investment decisions on their behalf.

Key VCT Benefits (2026)

- Income tax relief of 20% on qualifying new VCT shares issued on or after 6 April 2026.

- Annual investment limit of £200,000.

- Tax-free dividends.

- No Capital Gains Tax (CGT) on gains from VCT shares.

- Professional management and diversification.

- Shares trade on the London Stock Exchange.

VCT Holding Requirement

To keep the income tax relief, investors must generally hold VCT shares for at least five years. Selling earlier may result in HMRC reclaiming the relief.

| Also Read: High networth investment strategies for 2026 |

Understanding EIS

The Enterprise Investment Scheme allows you to make direct investments in qualifying small UK companies, with significant potential for growth, however there is a higher level of risk due to the nature of these businesses. You will hold shares directly, rather than through a pooled fund managed by a professional fund manager.

Key EIS Benefits (2026)

- 30% income tax relief on qualifying investments.

- Annual investment limit of £1 million, or £2 million if at least £1 million is invested in knowledge-intensive companies.

- Capital Gains Tax exemption after the qualifying holding period.

- Capital gains tax deferral relief.

- Loss relief if investments fail.

- Potential inheritance tax advantages through Business Relief.

EIS Holding Requirement

Investors must generally hold EIS shares for at least three years to retain tax benefits.

VCTs vs EIS: The core difference

| Aspect | VCTs | EIS |

|---|---|---|

| Structure | Pooled fund of 20-70 companies; pros manage it | Direct shares in 1+ early-stage firms; you pick |

| Income Tax Relief | 20% on max £200k/year (was 30% pre-2026) | 30% on max £1m (£2m knowledge-intensive) |

| Holding Period | 5 years to lock in reliefs | 3 years |

| Dividends | Totally tax-free | Taxed as normal income |

| CGT on Gains | 100% exempt | 100% exempt (plus deferral option) |

| Loss Relief | No | Yes |

| IHT Relief | No | Yes, after 2 years |

| Risk Feel | Smoother ride via diversification | Bumpier, but loss relief cushions blows |

| Investor Style | Passive, dividend seekers | Active, growth chasers with bigger |

| Also Read: How to build a high capital investment strategy for large portfolios |

2026 Tax Changes Impact

On April 6, UK Tax Changes 2026 will impact VCTs and EIS in an effort to balance support provided to VCTs and EIS against the need for fiscal sustainability. Under the new UK tax regime, the amount of income tax relief that investors in VCTs will be able to claim will be reduced from 30% to 20% of the annual maximum amount allowed.

This will result in a reduction in tax relief available at the outset for those making investments in funds seeking a passive method of diversification and that make tax-free distributions. The EIS will continue to provide the same level of income tax relief of 30%, thus retaining its position as an attractive investment option for individuals wishing to make a direct investment in a private company/start-up.

In addition to providing income tax relief for up to 30% of their investment in an EIS, investors are also able to claim any losses incurred through their investment as a means to offset against other taxable incomes after 2 years from the date of the investment, and to benefit from IHT after making their investment for a minimum of two years, EIS will allow for the doubling of the maximum funding amounts that can be raised annually and over the life of the company, and to increase the level of assets that the company has at any one time in order to attract further investment from EIS funds.

While the changes to the UK tax regime will move investors who were seeking to build a larger portfolio through VCTs into the use of EIS in order to obtain the same level of income tax relief, VCTs are still providing investors with reliable income streams at an affordable price. It’s a good idea to meet with your financial adviser to determine how best to achieve this goal.

Investment Risks and Returns

The fact that both VCTs vs EIS are high-risk investments as they support unlisted start-ups with most of them failing early on so there could be a full capital loss even if you receive some tax benefits. There is also mitigation to invest through VCTs which automatically diversify themselves across a range of companies so if one fails there are others to spread the loss over e.g., with EIS you select your own companies and therefore must make sure you spread your investment across more than one.

In terms of returns, when you receive tax relief on your investments, your capital costs will have been reduced prior to making the investments. You can also expect reasonable returns through both successful disposals and dividend payments with either a VCT or EIS being the better choice based on how aggressive of estate you desire. Finally, regardless of how you invest be sure to hold the investments for the long term, and if you want to lose an entire investment, consider speaking to an investment consultant before wasting your money.

VCTs vs EIS: Choosing Your High-Capital Strategy

If you are looking for a way to invest quickly and easily, go with VCTs as they allow you to invest in many new businesses managed by professional investors without worrying about taxes, and they pay out dividends without any effort on your part.

If you are seeking significant tax savings and want to make a large investment in a rapidly growing organization, select EIS investments directly in that company. Like VCTs, EIS provide significant assistance with inheritance taxes, so it is wise to invest across multiple EIS businesses to lower risk.

By doing this, you will get both growth (EIS) and income (VCT) in my opinion. However, don’t invest your entire portfolio into EIS or VCT until you speak with an investing consultant who can assist you in determining your financial objectives and tax liabilities.

Which Is Better for Capital Growth?

VCT May Suit You If:

- You want a hands-off investment.

- You prefer professional fund management.

- You value tax-free dividend income.

- You want diversification across many companies.

EIS May Suit You If:

- You are comfortable with higher risk.

- You want larger tax reliefs.

- You are targeting long-term capital growth.

- You have already used ISA and pension allowances.

- Estate planning is part of your investment strategy.

A Balanced Approach

Many high-net-worth investors use both schemes.

A common approach is:

- VCTs for tax-free income and diversification

- EIS for growth potential and enhanced tax reliefs

This allows investors to benefit from both income generation and long-term capital appreciation while spreading risk across different investment structures.

Final Thoughts

VCT and EIS offer a smart way to invest and reduce your taxable income, although there will be some changes from 2026 which may affect the amount of tax relief offered via VCT. Enterprise investment schemes (EIS) are also a good option for larger amounts of investments and for transferring wealth to future generations. Venture capital trusts allow you to withdraw cash without worry.

It is a good idea to invest in both for a mix of potential rewards from both and an exposure to the risk of investing in early stage businesses. According to me, you should seek the advice of a financial adviser, only use funds you can afford and don’t rush into anything; good things come to those who are patient.

FAQ’s on VCTs vs EIS

What is the main difference between VCTs and EIS?

VCTs are professionally managed funds that allow for easier diversification while providing tax-free income from dividends. EIS is when an individual will purchase shares in a single company directly, which provides greater tax relief; however, this method carries more risk because of being actively involved with the company.

Is VCT tax relief change in 2026?

Yes, it fell from higher levels to a lower rate.

Which is better for large investments?

According to my research EIS is better for large investments.

Do I need an adviser?

Yes you must take advise from experts on VCTs vs EIS.